DRS/A: Draft registration statement submitted by Emerging Growth Company under Securities Act Section 6(e) or by Foreign Private Issuer under Division of Corporation Finance policy

Published on December 11, 2023

As confidentially submitted to the Securities and Exchange Commission on December 8, 2023.

This draft registration statement has not been publicly filed with the Securities and Exchange Commission and all information herein remains strictly confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

IBOTTA, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 7310 | 35-2426358 | ||||||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

||||||

|

1801 California Street, Suite 400

Denver, Colorado 80202

303-593-1633

|

||||||||

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Bryan Leach

Chief Executive Officer and President

Ibotta, Inc.

1801 California Street, Suite 400

Denver, Colorado 80202

303-593-1633

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Larry W. Sonsini | David Boston | ||||

| Mark Baudler | Tej Prakash | ||||

| Melissa Rick | Willkie Farr & Gallagher LLP | ||||

| Seth Helfgott | 787 Seventh Avenue | ||||

| Rachel Nagashima | New York, New York 10019-6099 | ||||

| Wilson Sonsini Goodrich & Rosati, P.C. | 212-728-8000 | ||||

| 650 Page Mill Road | |||||

| Palo Alto, California 94304 | |||||

| 650-493-9300 | |||||

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

☐ | Accelerated filer |

☐ | ||||||||

Non-accelerated filer |

☒ |

Smaller reporting company |

☐ | ||||||||

Emerging growth company |

☒ |

||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission acting pursuant to said Section 8(a) may determine.

EXPLANATORY NOTE

Pursuant to the applicable provisions of the Fixing America’s Surface Transportation Act, we are omitting our unaudited financial statements as of and for the nine months ended September 30, 2023 and 2022 because they relate to historical periods that we believe will not be required to be included in the prospectus at the time of the contemplated offering. We intend to amend the registration statement to include all financial information required by Regulation S-X at the date of such amendment before distributing a preliminary prospectus to investors.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated , 2024

Shares

Class A Common Stock

This is an initial public offering of shares of Class A common stock of Ibotta, Inc. We are selling shares of our Class A common stock.

Following this offering, we will have two series of authorized common stock: Class A common stock and Class B common stock. The rights of the holders of Class A common stock and Class B common stock are identical, except with respect to voting and conversion rights. Each share of Class A common stock is entitled to one vote. Each share of Class B common stock is entitled to 20 votes and is convertible at any time into one share of Class A common stock. Upon completion of this offering, Bryan Leach, our Founder, Chief Executive Officer and President and member of our board of directors, and entities affiliated with Mr. Leach will hold approximately % of the combined voting power of our outstanding capital stock, assuming no exercise by the underwriters of their option to purchase additional shares of Class A common stock from us in this offering. As a result, Mr. Leach generally will be able to determine any action requiring the approval of our stockholders, subject to limited exceptions, including the election of our board of directors, the adoption of amendments to our certificate of incorporation and bylaws (where adopted by stockholders), and approval of any merger, consolidation, sale of all or substantially all of our assets, or other major corporation transactions.

Prior to this offering, there has been no public market for our common stock. It is currently estimated that the initial public offering price will be between $ and $ per share. We intend to apply to list our Class A common stock on the under the symbol “IBTA.”

We are an “emerging growth company” as defined under the federal securities laws and, as such, we have elected to comply with certain reduced public company reporting requirements for this prospectus and may elect to do so in future filings.

Investing in our Class A common stock involves risks that are described in the “Risk Factors” section beginning on page 21 of this prospectus.

| Per Share | Total | ||||||||||

Initial public offering price |

$ | $ | |||||||||

Underwriting discounts and commissions(1)

|

$ | $ | |||||||||

Proceeds, before expenses, to us |

$ | $ | |||||||||

______________

(1)See the section titled “Underwriting” for additional information regarding compensation payable to the underwriters.

To the extent that the underwriters sell more than shares of Class A common stock, the underwriters have the option to purchase up to an additional shares of Class A common stock from us at the initial public offering price less the underwriting discounts and commissions.

Neither the Securities and Exchange Commission nor any other state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of Class A common stock to purchasers on or about , 2024.

| Goldman Sachs & Co. LLC | Citigroup | BofA Securities | ||||||

Prospectus dated , 2024

TABLE OF CONTENTS

| Page | |||||

We and the underwriters have not authorized anyone to provide you any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for and can provide no assurance as to the reliability of any other information that others may give you. We and the underwriters are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations, and prospects may have changed since that date.

For investors outside of the United States: we have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of Class A common stock and the distribution of this prospectus outside of the United States.

GLOSSARY OF KEY TERMS

Throughout this prospectus, we use the following key terms:

Ad products. Paid digital advertisements such as banners, tiles, newsletters, and feature placements bought by clients to raise awareness of their offers and/or communicate their brand messages.

Application Programming Interface (API). A set of functions and procedures allowing the creation of apps that access the features or data of an operating system, app, or other service.

Artificial Intelligence (AI). Capabilities that leverage machine learning, deep learning, generative AI, and natural language processing on Ibotta’s technology platform.

Campaign. An organized course of action that clients undertake to promote a product or service on the IPN. A campaign may include one or more offers and related ad products.

Cash back. A form of reward that gives consumers a cash rebate after they purchase a product that qualifies for the reward.

Client. A company that pays Ibotta for the use of its performance marketing platform with the goal of influencing consumer purchase behaviors. A client can own one or multiple CPG brands.

Closed-loop. Any retailer loyalty or rewards program that generates a positive currency that is stored in a digital wallet or stored value account and which then can be spent back at the retailer. Closed-loop programs are an alternative to “open loop” techniques such as paper or digital coupons that give consumers a discount at checkout.

Consumer. An individual who purchases groceries or general merchandise, either online or in-store. If a consumer has accessed the website or downloaded an app of one or more publishers or visited a store of a publisher, such consumer may be counted as multiple consumers.

CPG brand (or brand). A CPG brand is an identifying name of a specific product or group of products owned by a company that sells consumer packaged goods, including in the grocery and general merchandise categories.

Digital offer program. A program that allows consumers to engage with offers on digital properties that could include a website, mobile app, mobile web interface, or some combination thereof.

Digital promotions. Offers, discounts, and cash-back rewards that are marketed through online-based digital technologies such as desktop computers, mobile phones, and other digital media.

Discount. A reduction in the price of a product or service applied at the time of the purchase.

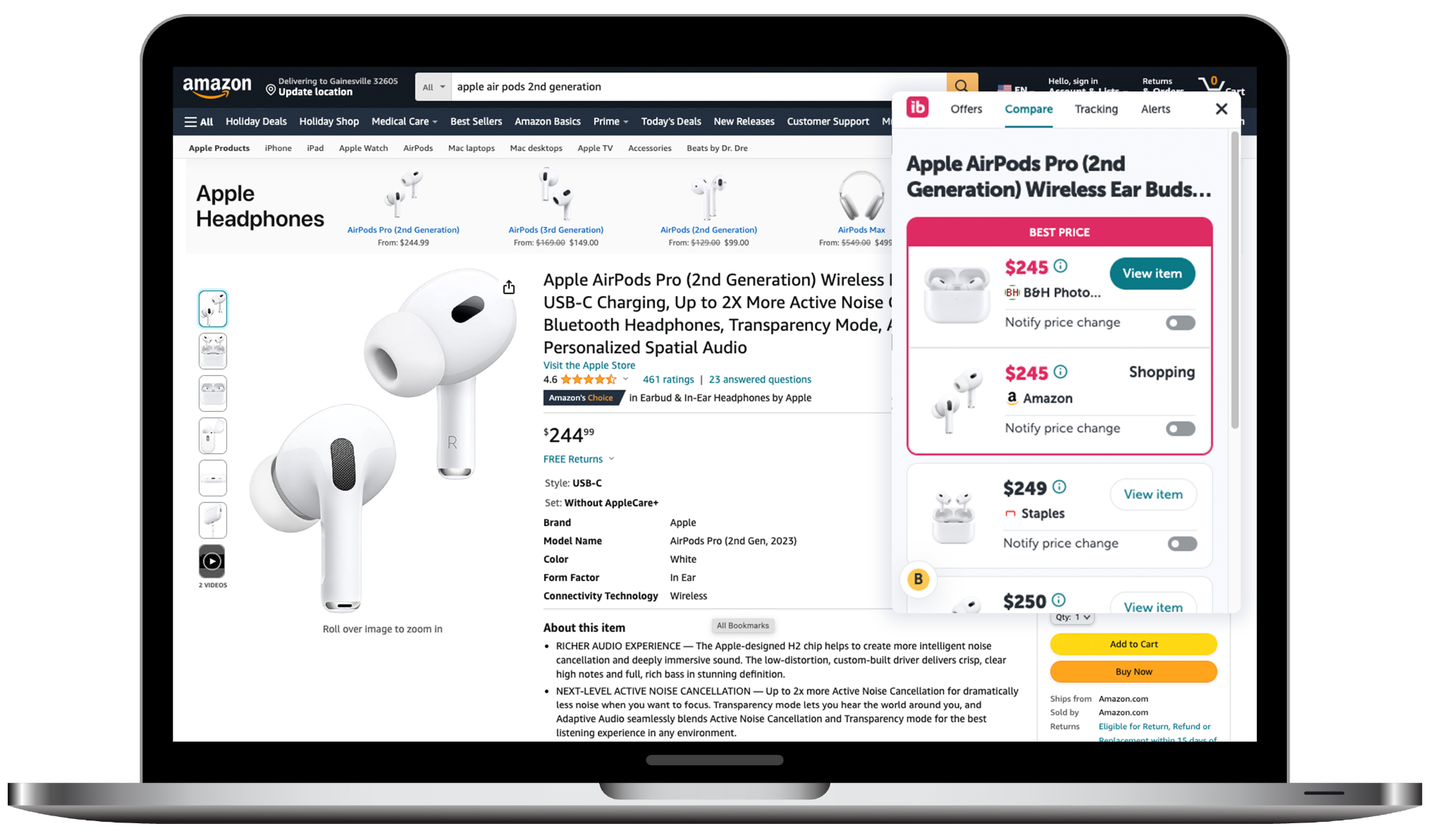

Ibotta Direct-to-Consumer (D2C). Ibotta’s direct-to-consumer products include a free mobile app, website, and browser extension that are branded through Ibotta and allow consumers to earn cash back rewards for everyday purchases.

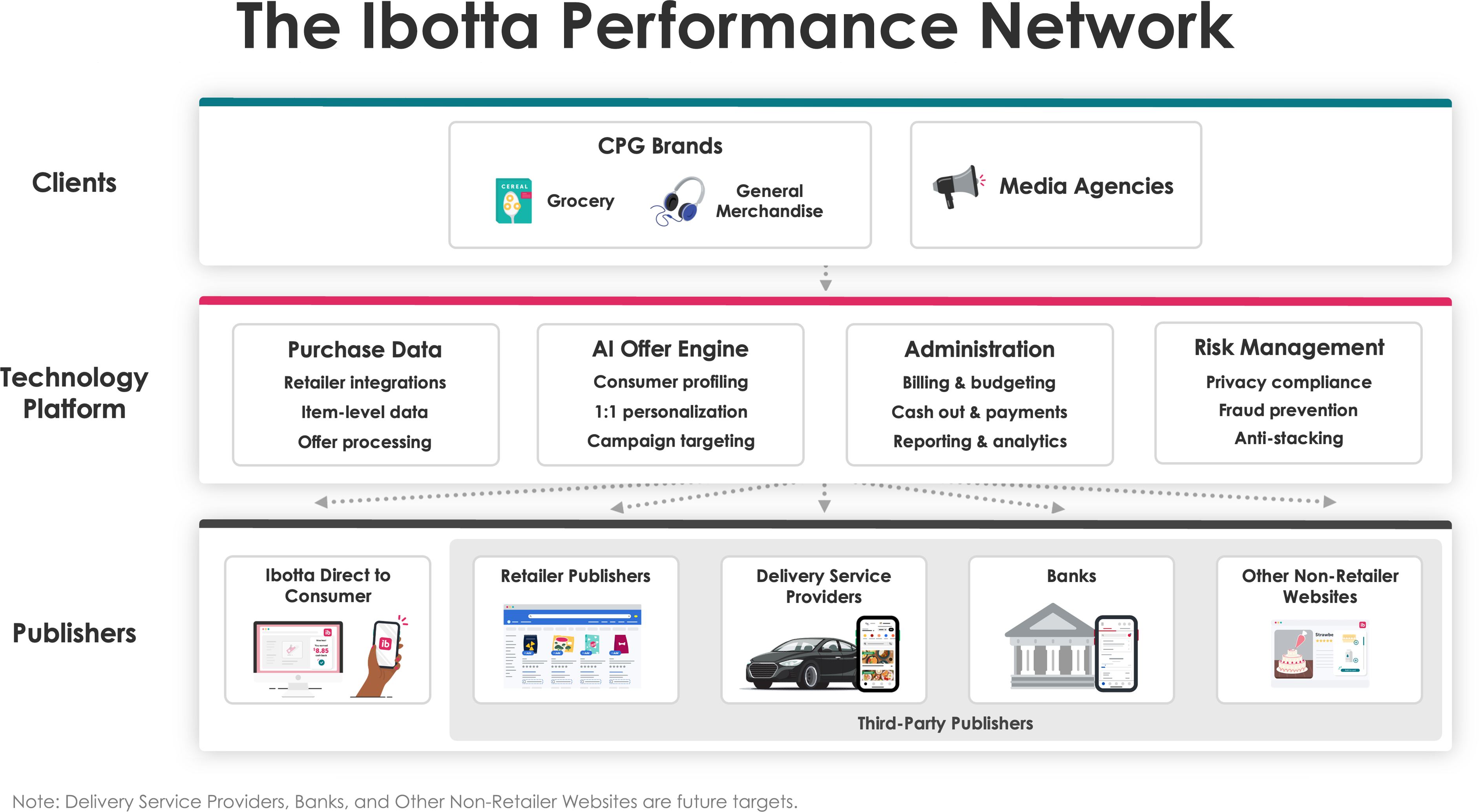

Ibotta Performance Network (IPN). An AI-enabled technology platform that allows CPG brands to deliver digital promotions to consumers via a network of publishers, in a coordinated fashion and on a fee-per-sale basis.

Integrated retailer. A retailer that sends item-level purchase data to Ibotta so that offers can be seamlessly redeemed in its stores or on its apps or websites.

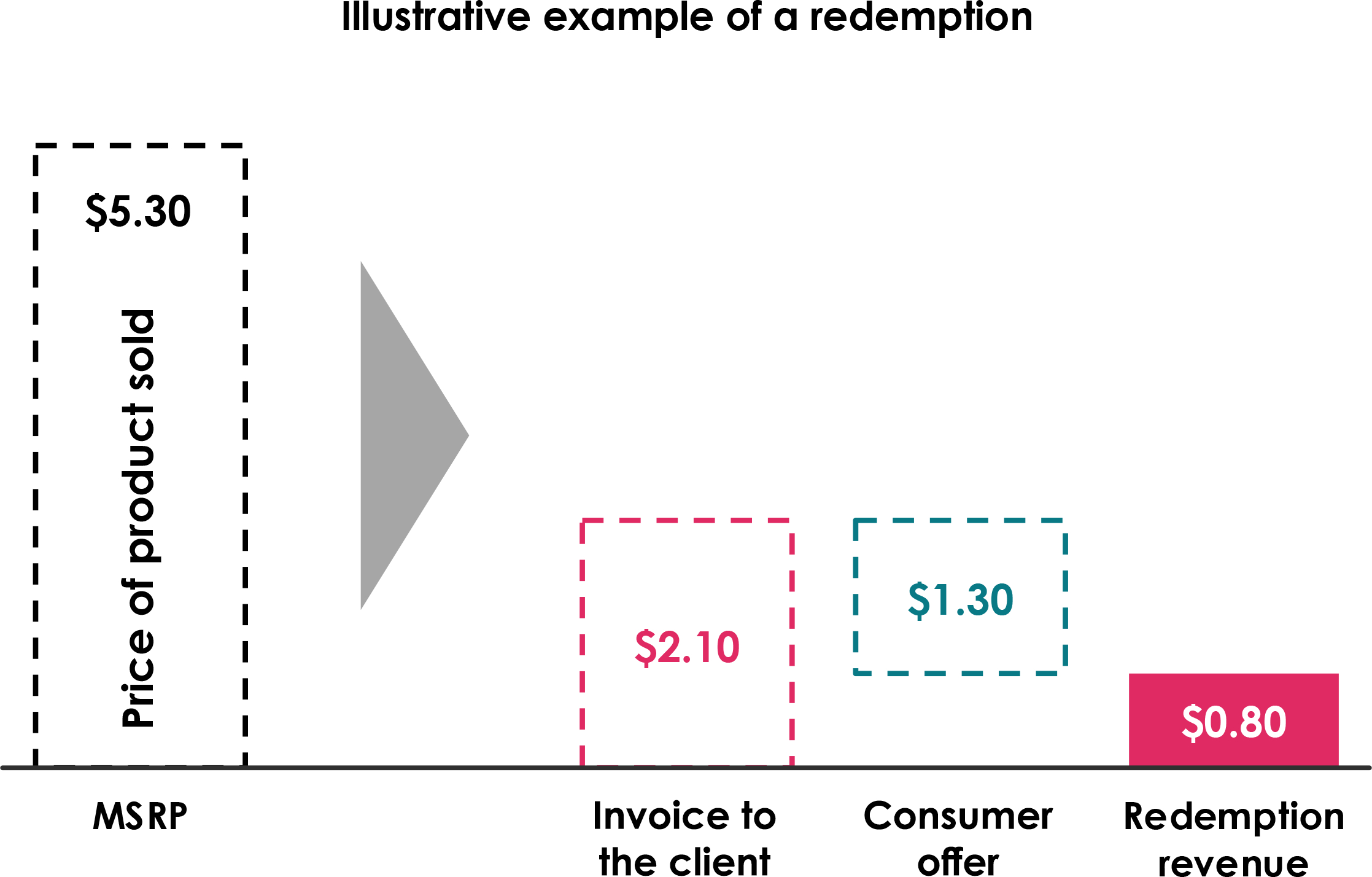

Manufacturer's Recommended Retail Price (MSRP). The price at which manufacturers recommend that retailers sell their product.

i

Offer. A digital promotion that encourages consumers to purchase one or more CPG brands or shop at a specific retailer in exchange for a reward or discount.

Offer stacking. The possibility for a consumer to locate the same offer on more than one publisher, make a single purchase, and earn rewards more than once for that offer.

Point of Sale (POS). A device or system that is used to process consumer transactions by retailers.

Publisher. A company that hosts Ibotta-sourced offers on its websites or mobile apps, as part of the IPN. Publishers include third parties that host Ibotta’s offers on a white-label basis (e.g., a retailer publisher such as Walmart), as well as Ibotta itself, which hosts its own offers on Ibotta D2C properties.

Redeemer. A consumer who has redeemed at least one digital offer within the quarter. If a consumer were to redeem on more than one publisher during that period, they would be counted as multiple redeemers.

Redemption. A verified purchase of an item qualifying for an offer by a client on the IPN.

Retail banner. A unique brand name of one retail store or a chain of retail stores owned by a retailer. A retailer may operate one or more retail banners.

Retailer. A parent company that owns and operates one or more physical or virtual stores under one or more retail banners that sell CPG brands to consumers. Retailer includes retailer advertisers, retailer publishers, and integrated retailers.

Retailer advertiser. A retailer that pays Ibotta a publisher commission when consumers click through to, and make a purchase from, the retailer’s website from one of Ibotta’s D2C properties. In some cases, Ibotta may also run promotions funded by retailer advertisers that encompass both online and offline sales, meaning consumers can earn cash back as a percentage of their total in-store basket spend, or as a percentage of their total online basket.

Retailer-exclusive marketing. Marketing dollars that CPG brands designate for the purpose of helping drive sales within one specific retailer environment, sometimes referred to as “shopper marketing.”

Retailer publisher. A retailer that is also a publisher on the IPN, meaning it hosts Ibotta-sourced offers on its digital properties.

Return on Ad Spend (ROAS). A common marketing metric used by CPG brands and other advertisers that measures sales earned for each dollar spent on advertising.

Reward. Value or credit provided to a consumer upon the successful redemption of an offer, which may take the form of cash back, points, or other loyalty currency.

Third-Party publisher. A non-Ibotta D2C publisher that hosts Ibotta-sourced offers on its digital properties and is part of the IPN, e.g., major retailer publishers such as Walmart, Dollar General, and Kroger.

Universal Product Code (UPC). A number that uniquely identifies each product sold by retailers. Each offer specifies which UPCs are eligible for redemption.

White-label. An arrangement that allows publishers to leverage our technology and offers to power their loyalty program without Ibotta’s brand.

ii

LETTER FROM BRYAN LEACH, FOUNDER & CEO

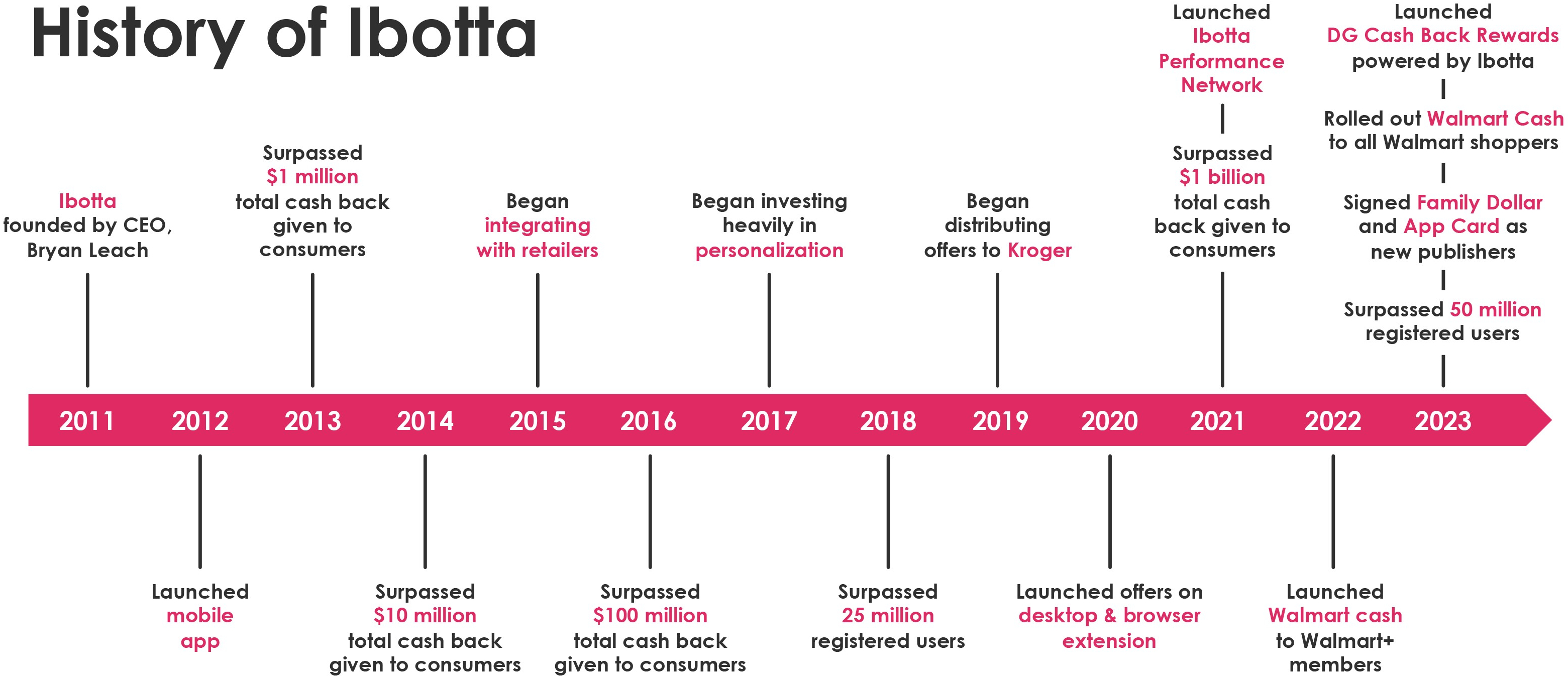

In 2011, I was flying back from a legal conference on international arbitration in Rio de Janeiro, Brazil when I saw a woman on the plane taking a picture of her receipts to submit her expenses for reimbursement. It made me think about the power of all the data contained on a receipt: detailed information about everything we buy, including the UPC, price, and quantity of every item in the basket, along with the date, time, retailer, and store location of purchase. It was a treasure trove of information, but until then, there had been no way to organize the information into an accurate picture of a person’s spending habits across all the places they shop. If technology could allow us to harness that data to create a granular understanding of purchase behavior, how could that transform the way that promotions and advertisements are delivered? How could companies get smarter about convincing consumers to change their purchase habits in the grocery store and beyond? In those musings lay the kernel of Ibotta (“I-bought-a”), which I hoped might one day help millions of consumers earn rewards for trying new brands, while at the same time reshaping the future of digital marketing. My journey from that moment to the present has involved many twists and turns, but one motivation has remained: the desire to be part of a team that creates something that directly helps people in their everyday lives. Not just people who have means, but people who will use what we built to help pay for food, rent, medical bills, student debt, vacations, and gifts for their children at the holidays.

In the United States today, 60% of adults are living paycheck to paycheck. Nearly three-quarters say they are not financially secure, and over a quarter expect that they will never be financially secure. Persistent inflation has only made matters worse. For millions of American families, the ability to make ends meet depends on their capacity to save money wherever and whenever they can. 87% of consumers’ grocery purchases are influenced by offers, discounts, and promotions. Digital promotions now make up the majority of all consumer promotions, with paper promotions in rapid decline. In-store sales still comprised 88% of grocery sales in the $1.1 trillion grocery sector in 2022, but consumers expect to find value regardless of whether they shop in-store, buy ahead and pickup in-store, or shop online with delivery.

At Ibotta, our mission is simple: Make Every Purchase Rewarding. Consumers earn millions of dollars in cash back rewards on their everyday purchases by interacting with our mobile app and website, and through the programs we power behind the scenes for third-party publishers. Unlike other forms of advertising, we cut consumers in on the deal, meaning whenever someone buys a product in response to a promotion, we pass along a portion of our advertising fee in the form of a reward. Because our offers are 100% digital, we can target promotions not merely based on what websites they have visited or where or when they have shopped, but based on which specific items they have bought in the past across a wide range of retailers, in-store or online. And we can tie everything out to a sale.

Our journey reflects our desire to reward as many purchases as possible. We began by releasing our own cash back mobile app in October 2012. Since then, it has attracted over 50 million registered users and more than 2.3 million ratings across the App Store and Google Play Store, earning an average of 4.7 out of 5 stars. In 2020, we began building the Ibotta Performance Network (IPN) with the goal of dramatically expanding our scale by distributing our exclusive offers on various third-party digital properties. Making every purchase rewarding meant not only operating under our own brand but also taking the technology and infrastructure we had built, and our exclusive offers, and making it all available on a white-label basis to publishers that wanted a plug and play technology solution. A significant portion of our offer redemptions now occur on third-party publishers that leverage our technology platform and offers. Today, millions of consumers redeem our offers on Walmart, Dollar General, Kroger, Shell, and other retailer properties without ever creating an Ibotta account or downloading our app.

Thousands of CPG brands rely on Ibotta to help them promote their products through the use of digital incentives. Instead of asking our clients to pay us a fee based on the number of impressions, clips, or clicks we deliver, we ask them to pay us only when their campaign results in a confirmed sale of their product, either in-store or online. We are accountable for the bottom of funnel results; our clients do not bear the risk of underperformance. In a world where one can trace a digital interaction all the way out to

1

an in-store or online sale, we believe that the rationale for selling ads or promotions on anything other than a fee-per-sale basis is weaker than ever.

The desire for new forms of digital marketing that offer greater certainty of results and higher conversion is nearly universal. Therefore, we have not limited ourselves to helping CPG brands in the grocery category. Today, we work with many leading CPG brands in other categories such as toys, clothing, beauty, electronics, pet, home goods, and sporting goods. Companies in these categories have historically had limited access to true, omnichannel fee-per-sale marketing tools. Our AI-enabled technology platform aims to give them an easy way to reach the right consumers with the right incentive at the right time, based on their specific marketing objectives, at a scale previously unattainable in the digital promotions industry. Our tools allow them to track campaign performance and measure offer redemptions across multiple retailers simultaneously, all while remaining within a fixed budget and avoiding common pitfalls such as offer stacking.

We take pride in knowing that so many CPG brands have been with us since the beginning and continue to spend more with us each passing year. And yet, we have barely scratched the surface of our potential addressable market. We capture less than one percent of the approximately $200 billion that CPG brands spend annually to shape consumer purchase behaviors.

Ibotta’s success has been fueled by our strong culture. We take pride in our mission, which helps people in a very concrete way. We live by our “IBOTTA” values: Integrity, Boldness, Ownership, Teamwork, Transparency, and A Good Idea Can Come From Anywhere. We foster an inclusive environment that welcomes diverse experience, backgrounds, lifestyles, and perspectives. We hold a high bar for performance. Among the many benefits we offer, we believe the most valuable is the opportunity to solve challenging problems with dedicated colleagues every single day.

The Ibotta experiment began twelve years ago in the windowless basement of an old fire station in downtown Denver. Our capital-light business has allowed us to grow rapidly while increasing profitability over time and capturing the benefits of a multi-sided network that we believe is very hard to replicate. So far, we have given over $1.6 billion in cash back to U.S. consumers on their everyday purchases, but we’re just getting started.

I hope you’ll decide to join us!

Bryan Leach

2

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus and is qualified in its entirety by the more detailed information and consolidated financial statements included elsewhere in this prospectus. It does not contain all of the information that may be important to you and your investment decision. You should carefully read this entire prospectus, including the sections titled “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our financial statements and related notes included elsewhere in this prospectus. In this prospectus, unless context requires otherwise, references to “we,” “us,” “our,” “Ibotta,” or the “Company” refer to Ibotta, Inc. and its wholly-owned subsidiary and references to “common stock” include our Class A common stock and Class B common stock.

Overview

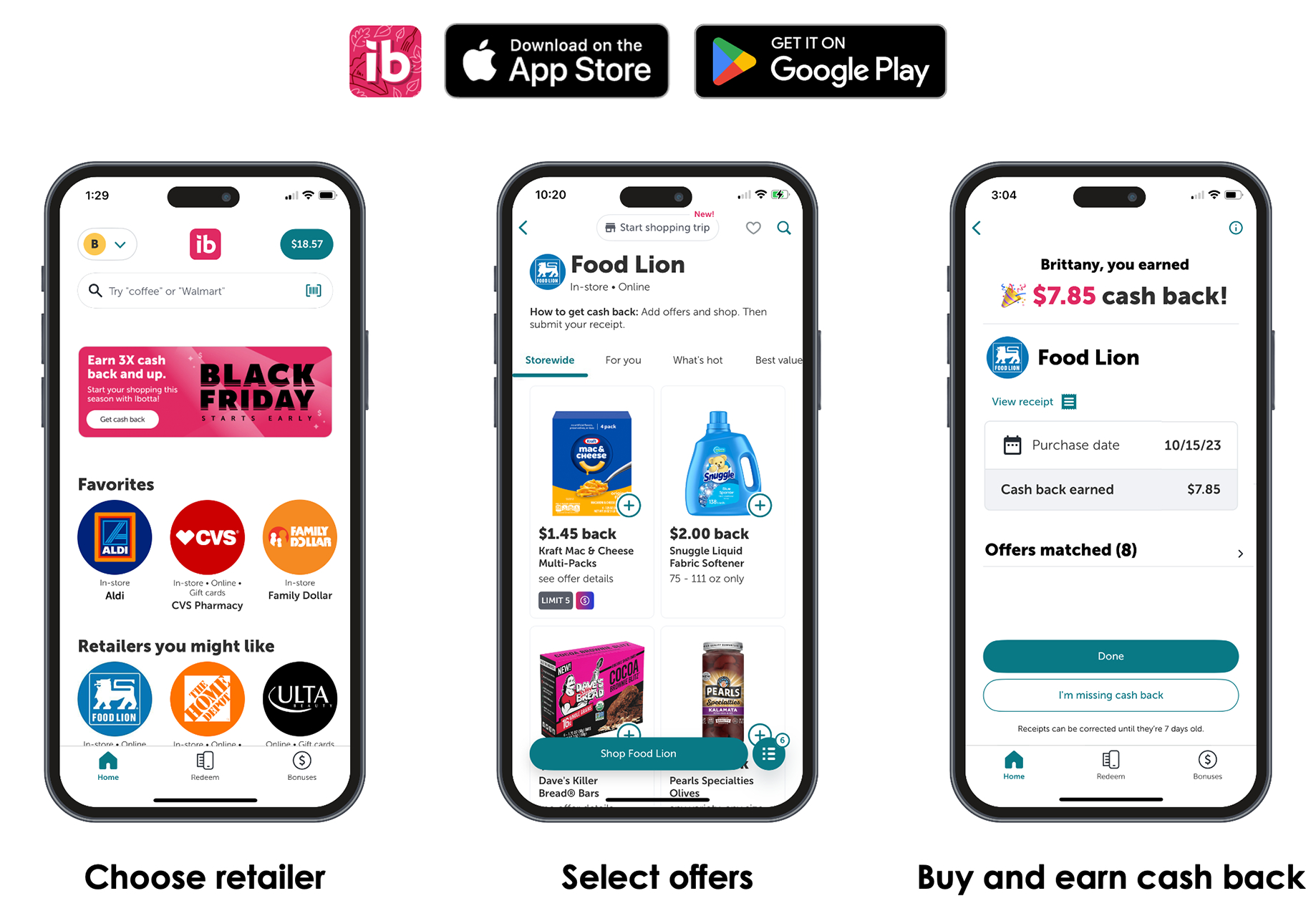

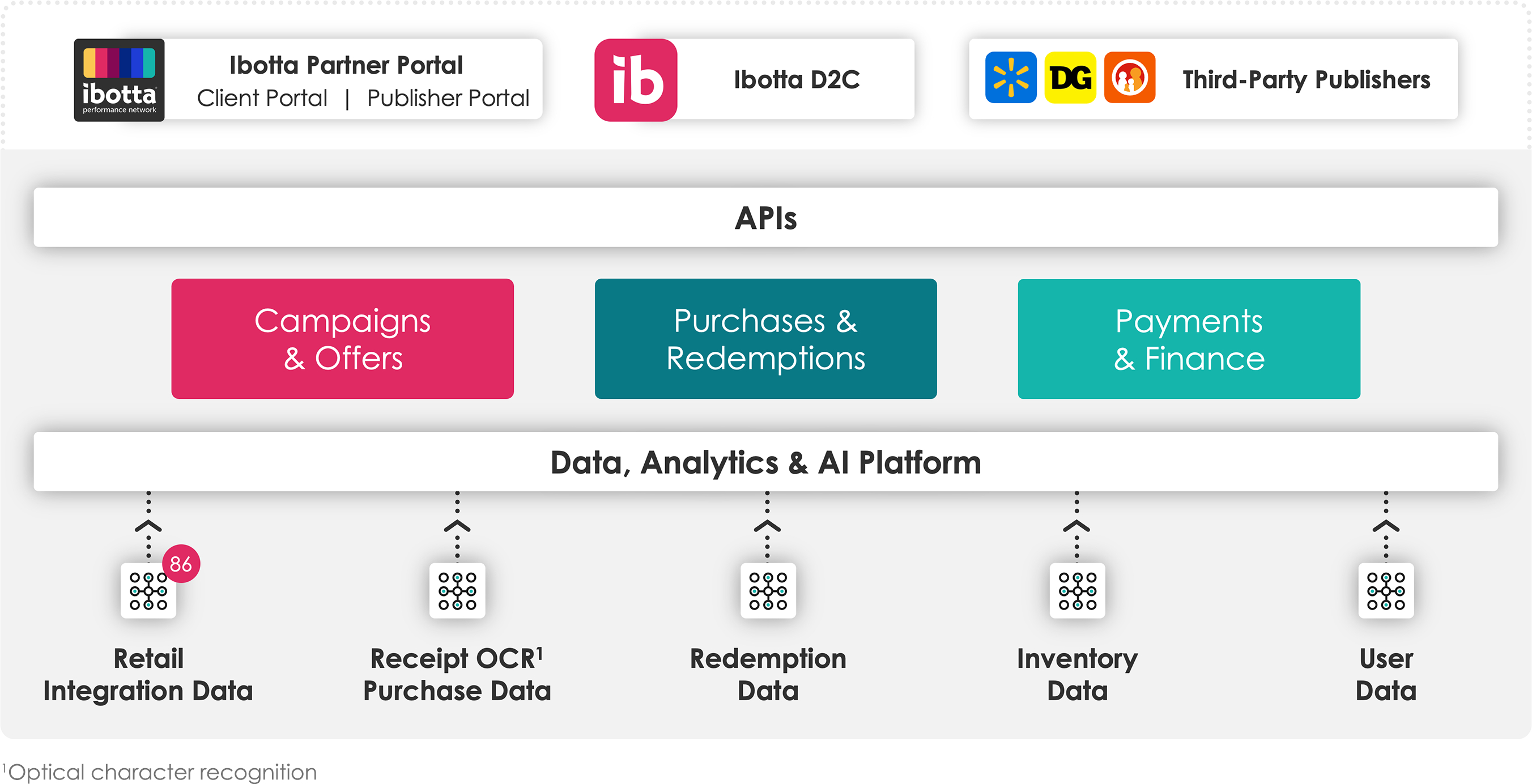

Ibotta’s mission is to Make Every Purchase Rewarding. Our technology allows CPG brands to deliver digital promotions to over 200 million consumers through a single, convenient network called the Ibotta Performance Network (IPN). We are pioneers in success-based marketing: we only get paid when our client’s promotion results in a sale, not when a consumer merely views or clicks on the promotion. We have built the largest digital item-level promotions network in the United States by forming strategic relationships with major retailers such as Walmart Inc. (Walmart) and Dollar General Corporation (Dollar General), which use our digital offers to power their loyalty programs on a white-label basis. Through the IPN, our clients can also reach millions more consumers on our widely used rewards app digital properties, which include the Ibotta-branded cash back mobile app, website, and browser extension (collectively, Ibotta D2C).

We work directly with over 750 different clients, representing over 2,250 different CPG brands to source exclusive offers. Most of our offers cover products in non-discretionary categories, such as grocery, but we also work with general merchandise manufacturers in categories such as toys, clothing, beauty, electronics, pet, home goods, and sporting goods. Over time, our clients have generally ramped up their spend with us, and they rarely drop off our network. In fact, of our top 100 clients, 99% were retained from 2021 to 2022.

Our technology platform uses an Artificial Intelligence (AI)-enabled offer engine that is designed to match and distribute the right offer to the right consumer at the right time. This is possible because we receive a large volume of item-level purchase data through our secure point of sale (POS) integrations with 86 different retailers. Using this data, we form a profile of each consumer based on what they have bought in the past and how they have responded to various price promotions. From there, we build recommenders that are driven by machine learning and designed to create personalized savings experiences for each consumer. The more data we accumulate, the smarter our recommenders become. Whatever our clients’ specific objectives may be – such as encouraging brand switching, shortening purchase cycles, incentivizing consumers to stock up, or promoting around key seasonal events – our platform helps them design a promotional campaign to accomplish their goals.

Ibotta’s technology tracks which offers are selected by consumers, matches offers to the products that have been purchased, logs redemptions, handles the flow of funds, and takes care of all downstream billing and logistics. We perform the function of “air traffic control,” meaning our network enables offers to be matched, distributed, and redeemed across multiple large third-party publishers in a coordinated fashion. This minimizes the risks that offer budgets are exceeded and that consumers redeem the same offer several times for a single purchase (i.e., offer stacking). Our client tools allow CPG brands to set up campaigns, monitor redemption and budget levels, and analyze overall campaign performance – all in a single, convenient interface.

We deliver success-based digital promotions at-scale because we manage a growing, open network of third-party publishers that host our offers. Retailers are among our most important publishers because their apps and websites are frequently visited by consumers with high purchase intent. A retailer may

3

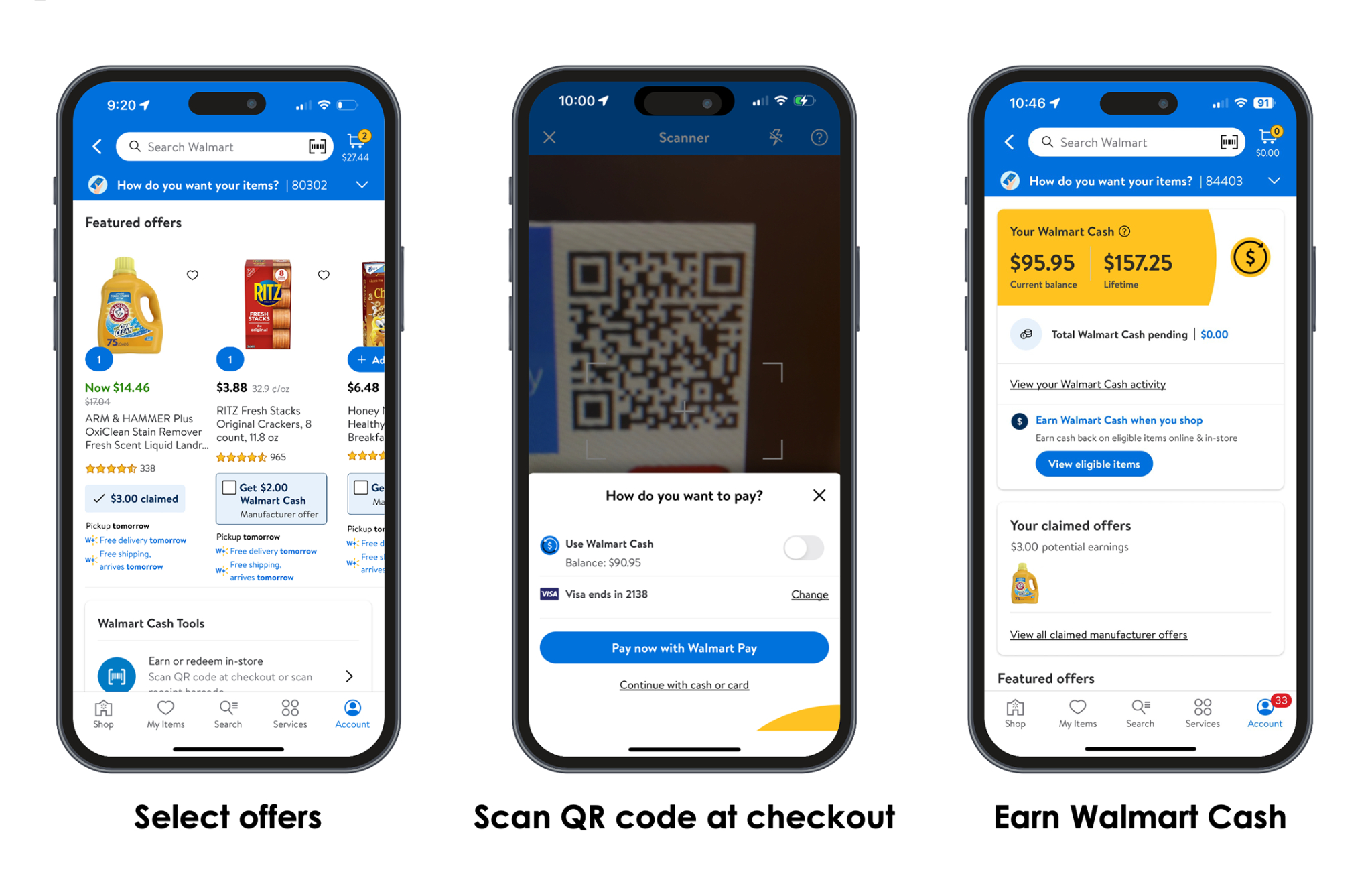

ingest digital offers from Ibotta’s Application Programming Interface (API) and present them to its consumers as part of its own branded loyalty program. We call these partners “retailer publishers.” We believe retailer publishers choose to work with Ibotta because we are a trusted partner that can provide a large universe of exclusive offers coupled with a set of plug and play capabilities that would be difficult for them to create and scale on their own. For example, Ibotta and Walmart entered into a multi-year strategic relationship that makes Ibotta the exclusive provider of digital item-level rebate offer content for Walmart U.S., across all product categories, for online and offline shopping. Consumers redeem our offers on Walmart properties without ever creating an Ibotta account. Instead, they can select manufacturer offers from the Walmart website or app, buy the featured items in-store or online, and instantly earn Walmart Cash which can be applied to future purchases in a Walmart store or on Walmart.com. All CPG brands wishing to run digital item-level rebates on Walmart’s website can only do so through the IPN.

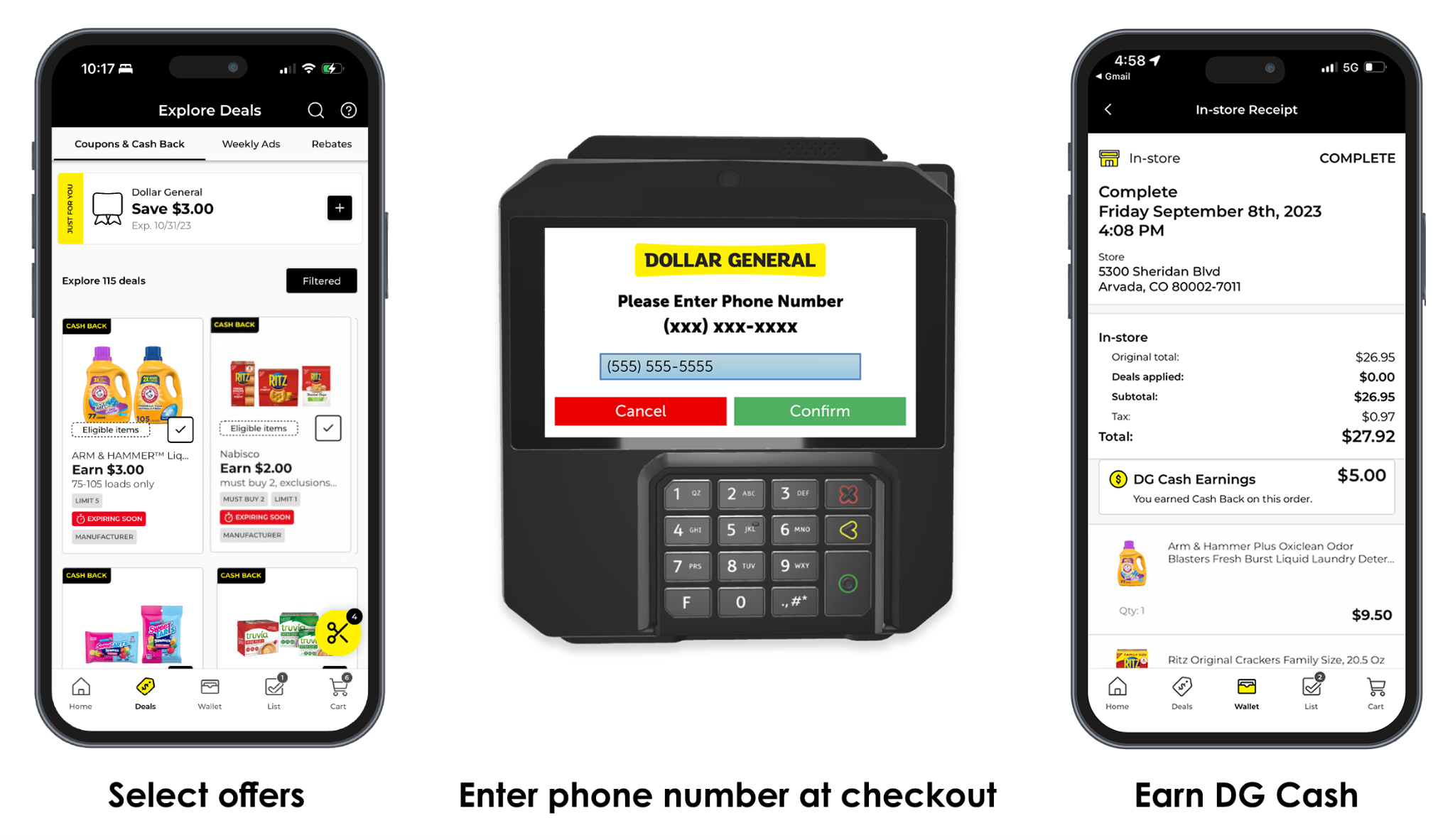

Ibotta also partners with several other leading retailer publishers. For example, Dollar General, the leader by market share in the dollar channel and one of the fastest growing retailers in the United States, began hosting Ibotta’s cash back offers in 2023. The DG Cash program represents Dollar General’s first foray into closed-loop item-level rewards, meaning offers, when redeemed, create a DG Cash currency that can be spent on future trips to Dollar General. The program is available to all users of the Dollar General mobile app and website, an audience that is price sensitive and focused on finding digital offers. Ibotta similarly partners with Family Dollar, a retail banner of Dollar Tree, Inc., who is in the process of becoming an IPN publisher. We also work indirectly to publish offers on certain retailer properties, including Kroger (powering Kroger Cash) and Shell (powering Shell Fuel Rewards).

In addition to providing digital offers for retailers, Ibotta also makes the same offers available on its own digital properties, which include Ibotta D2C. Since 2012, over 50 million Americans have registered for our free app. Ibotta D2C reaches a highly engaged audience of savings-conscious consumers who want a single digital starting point where they can find cash back offers across a variety of retailers. Many of these consumers decide where to shop based on the availability of deals in different retailers. Once the IPN launched, Ibotta D2C became a publisher on the IPN, meaning it is now one of many nodes through which our digital offers are delivered to the end consumer.

In the future, we believe the IPN may be extended to other publishers across a variety of new verticals. For example, new publishers could include delivery services, banks, or other apps and websites that want to give their consumers access to offers on popular everyday items without having to source those offers from thousands of different CPG brands or secure item-level data from multiple integrated retailers where the offers can be redeemed.

We believe Ibotta is well positioned to capitalize on a large and growing market opportunity. U.S. consumers spent an estimated $1.1 trillion dollars in the grocery sector in 2022. CPG brands compete fiercely to influence consumer spending habits, spending approximately $200 billion on marketing annually in the United States. In fact, no other industry spends more on marketing, as a percentage of overall budgets, than CPG.

Most of our revenue is redemption revenue which is generated from redemptions of offers across the IPN. A significant portion of that redemption revenue arises from offer redemptions on third-party publishers. We also generate revenue by selling ad products on our Ibotta D2C properties. Specifically, we allow CPG brands and retailers to enhance awareness of their offers by buying display ads, in-app videos, or email marketing campaigns. We also charge partners a licensing fee to leverage our aggregated data in ways that help them better understand their target consumers and improve their promotional activities. Finally, on Ibotta’s D2C properties, we also allow thousands of online retailers to advertise and present consumers with their own sitewide cash back offers. These clients benefit from the incremental sales generated by Ibotta’s savings-conscious audience.

Our revenue growth significantly accelerated with the addition of new publishers to the IPN. Most recently, the rollout of our offers on the digital properties of Walmart and Dollar General has attracted

4

larger audiences, and in turn, resulted in greater spend by CPG brands and a greater number of redeemed offers. These developments have increased our scale, growth and profitability.

•Total revenue grew from $210.7 million in 2022 to $ million in 2023, an increase of %;

•Redemption revenue grew from $138.7 million (or 66% of total revenue) in 2022 to $ million (or % of total revenue) in 2023, an increase of %;

•Gross profit grew from $164.5 million in 2022 to $ million in 2023, an increase of %;

•Net loss decreased from $54.9 million in 2022 to $ million in 2023; and

•Adjusted EBITDA margin improved from (13)% in 2022 to % in 2023.

Industry Background

CPG brands have long sought the ability to advertise or promote their products in a way that can be directly measured out to a sale and tied back to a known consumer. Having this capability would allow a CPG brand to prioritize investing in tactics with the highest observable conversion to sale in-store or online, present a different message or promotion to each segment of consumers, and pay only when the campaign succeeds in driving a sale.

As far back as 1880, CPG brands such as Coca-Cola looked for ways to entice consumers to try their products. They invented manufacturer coupons to address this challenge. Ever since, paper coupons and free-standing inserts (FSIs) have been printed and distributed in newspapers, cut out or “clipped” by consumers, presented at checkout in exchange for a discount on qualifying products, and then gathered up by retailers and shipped off to coupon clearinghouses. The use of paper coupons peaked in 1999, when approximately 340 billion of them were circulated in U.S. newspapers.

Paper coupons have several obvious drawbacks, however. First, rapidly declining newspaper circulation, particularly among younger consumers, has severely constrained their reach. Second, they often require CPG brands to take a one-size-fits-all approach by providing the same discount to everyone, regardless of their past purchase behaviors. Third, paper coupons suffer from very low redemption rates due to high friction in the redemption experience, including clipping a coupon, remembering to bring that coupon to the store, and presenting that coupon to the store clerk at checkout. Fourth, because of the cost to produce and distribute paper coupons, they are billed on a fee-per-print basis, meaning the brand is asked to pay a fixed rate based on the number of coupons circulated in print, regardless of whether conversion to sale ends up being low or high. Lastly, paper coupons harm the environment by causing millions of trees to be cut down unnecessarily each year, only to have 99.5% of the coupons go unused. Despite these significant drawbacks, paper coupons account for almost all of promotion volume.

About 20 years ago, print-at-home and load-to-card digital coupons began to address certain deficiencies of paper coupons. Digital coupons could be delivered via more modern distribution channels such as email, websites, and mobile apps, and they could be tailored to individuals based on their specific purchase patterns. But digital coupons still left much to be desired. Most notably, they were still billed on a fee-per-clip basis, meaning the CPG brand was charged as soon as a consumer activated an offer, regardless of whether they went on to purchase anything. The performance of these campaigns also often could not be measured by CPG brands in real-time, leaving them unable to optimize programs mid-flight. Equally problematic, digital coupon programs did not provide a way to deliver promotions nationally – i.e., across retailers – in the same way that paper manufacturer coupons had done. Instead, each retailer ran its own load-to-card program, and CPG brands could only run retailer-specific offers through those siloed programs.

Retailers also experienced challenges with digital coupons. Whenever a redemption occurred, they still had to forego the full retail price of a product and seek reimbursement via a clearinghouse. This maintained the negative working capital dynamics inherent in any discounting system. Additionally, digital

5

coupons remained entirely open loop, meaning all the savings dissipated instead of being internalized in the form of positive currency that had to be spent back at the same retailer on a future trip.

As the promotions industry has evolved, one feature has remained constant: the need for a third-party to manage offer distribution on behalf of all CPG brands and retailers in the ecosystem. This need persists for several reasons, including:

•Efficiency. It is inefficient for a CPG brand to negotiate, set up, and coordinate delivery of offers with each retailer that carries its products or each publisher that hosts its content.

•Scale. CPG brands and retailers need to reach the widest possible audience, including potential new consumers who do not belong to their loyalty programs or visit their apps and websites.

•National content. CPG brands generally have large national budgets that are reserved for platforms that can deliver promotions across multiple retailers. If a single retailer were to source its own offers, it would immediately be confined to the smaller retailer-exclusive marketing budgets set aside by a CPG brand for use with just that retailer.

•Coordination. CPG brands must ensure that their offers cannot be stacked across multiple publishers. To achieve this, there needs to be a single third-party network administrator that performs an “air traffic control” function, keeping track of which offers have been used on which publishers, in what order, and where credit has already been awarded so that it cannot be given a second time for the same purchase.

•Technological capability. CPG brands are experts in developing and marketing new products. Retailers are experts in merchandising, product placement, supply chain management, and retail operations. Neither is likely to have the time, expertise or desire to develop the necessary technology, including the tools to manage offer setup, design and optimization, AI-powered recommenders, digital wallet technology, billing, fraud prevention, and so forth.

Like promotions, advertising has also evolved to better meet the CPG brand’s needs over time. Traditional television, radio, and out of home are all tactics that reach a mass audience but do not enable precise targeting or direct measurement. Over time, new alternatives emerged which offered greater precision and measurability. Digital ad platforms, including walled gardens such as Google and Meta and independent demand-side platforms such as The Trade Desk, allow CPG brands to target ads primarily based on what websites a consumer has visited, online searches they have conducted, social pages they have liked, or connected television programs they have watched.

While the scale of these platforms is compelling, they continue to fall short in many regards. First, despite the growth of online grocery shopping, in-store sales still comprised 88% of grocery sales in 2022. Ad platforms optimized for online conversion work well where consumers frequently click through and buy products or services online. But in the CPG industry, where products are largely purchased in-store and transacted online far less frequently, these platforms are less effective. Second, CPG brands prefer to target ads using data about past purchases to measure the actual incremental sales lift generated by their ads. Digital ad platforms do not have access to cross-retailer, item-level purchase data that can be tied back to the individual consumer who viewed the ad to measure changes in purchase behavior over time. Third, recent privacy policies implemented by Apple, along with the imminent phase out of third-party cookies on Google’s Chrome browser, threaten to constrain advertisers’ future ability to target ads as effectively because consumers have little incentive to opt into sharing their data for the purpose of receiving more targeted display ads. Finally, and perhaps most importantly, digital ad platforms do not offer success-based billing in the sense that they charge for impressions and clicks rather than on a fee-per-sale basis.

Many CPG brands prefer to shift spend lower down in the funnel toward fee-per-sale based tactics because they can guarantee a desired level of return on ad spend (ROAS). Historically, the main

6

limitation has been that CPG brands lacked a fee-per-sale platform that could deliver digital promotions nationally and at a massive consumer scale.

Market Opportunity

U.S. consumers spent an estimated $1.1 trillion in the grocery sector in 2022. American consumers purchased groceries 1.5 times per week spending $438 per month in 2021, on average. Despite the growth of online grocery shopping, 88% of all grocery sales were made in physical stores in 2022.

We began by focusing on grocery because consumers purchase groceries at a higher frequency, which gives us an opportunity to influence consumer purchase habits on a weekly basis. Companies in the CPG industry spend a higher percentage of their gross sales on marketing than companies in any other industry. In 2022, total annual CPG marketing spend reached approximately $200 billion in the United States, of which approximately $172.5 billion was spent on trade promotions, digital, consumer promotions, and retailer-exclusive marketing. Total spend on digital rebates grew 26% year-over-year in the first half of 2022, and the digital promotions market is projected to grow at an 18.5% compound annual growth rate from 2023 to 2030.

The Ibotta Performance Network

The IPN provides an at-scale success-based marketing solution for the CPG industry. By using the IPN, CPG brands and their media agencies can create digital offers and match and distribute them in a coordinated manner across multiple publisher properties. These publishers include large retailers, which display our offers on their websites, as well as Ibotta’s D2C properties, which consist of our mobile app, website, and browser extension, which are popular tools for savings-oriented consumers. The IPN is powered by our proprietary, AI-enabled technology platform, which takes advantage of a unique set of purchase data that we receive through POS integrations with retailers.

The key components of our network are as follows:

Offer sourcing. Ibotta’s sales team directly sources digital offers from over 2,250 different CPG brands, and in some cases their media buying agencies.

7

Technology platform. Our cloud-based, AI-driven technology platform is built on an open architecture that enables us to deliver millions of offers from CPG brands to consumers across our network of publishers. The key components of this platform include:

•Purchase data. We receive and process a large amount of item-level consumer purchase data from our retailer POS integrations and use that data to process offer redemptions and help drive high return on investment outcomes for CPG brands.

•AI offer engine. We help our clients determine the optimal offer value, offer cadence, offer breadth, and targeting criteria for a given campaign, based on their strategic objectives. Using AI, we build recommenders that are designed to match the right offers with the right consumers at the right time. With machine learning, our recommendation algorithms continuously improve, allowing us to drive higher conversion and cost efficiency for our clients.

•Administration. We handle all aspects of billing and collections, as well as managing cash flows. We also provide our clients with a portal that allows them to set up and refine their offer parameters, as well as monitor and analyze their campaign performance.

•Risk management. We help minimize offer stacking by ensuring that a consumer who earns a reward for redeeming an offer on Ibotta’s app cannot earn a second, redundant reward on a third-party publisher for the same underlying purchase.

Distribution via publishers. We match and distribute our digital offers through retailer publishers and Ibotta D2C properties, with additional distribution channels planned for the future. We have formed strategic, and in some cases, exclusive relationships with large retailers such as Walmart, Dollar General, and Family Dollar.

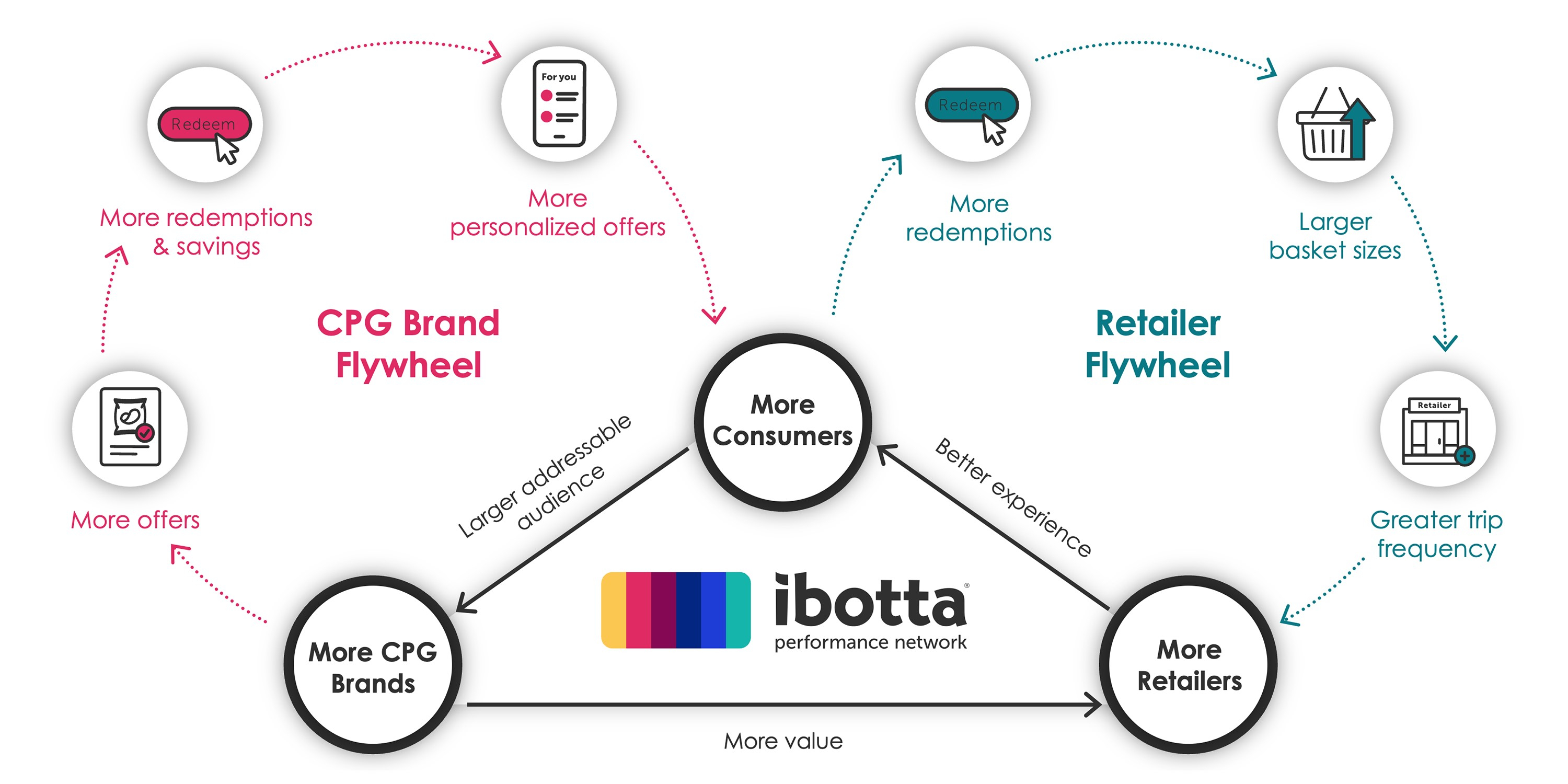

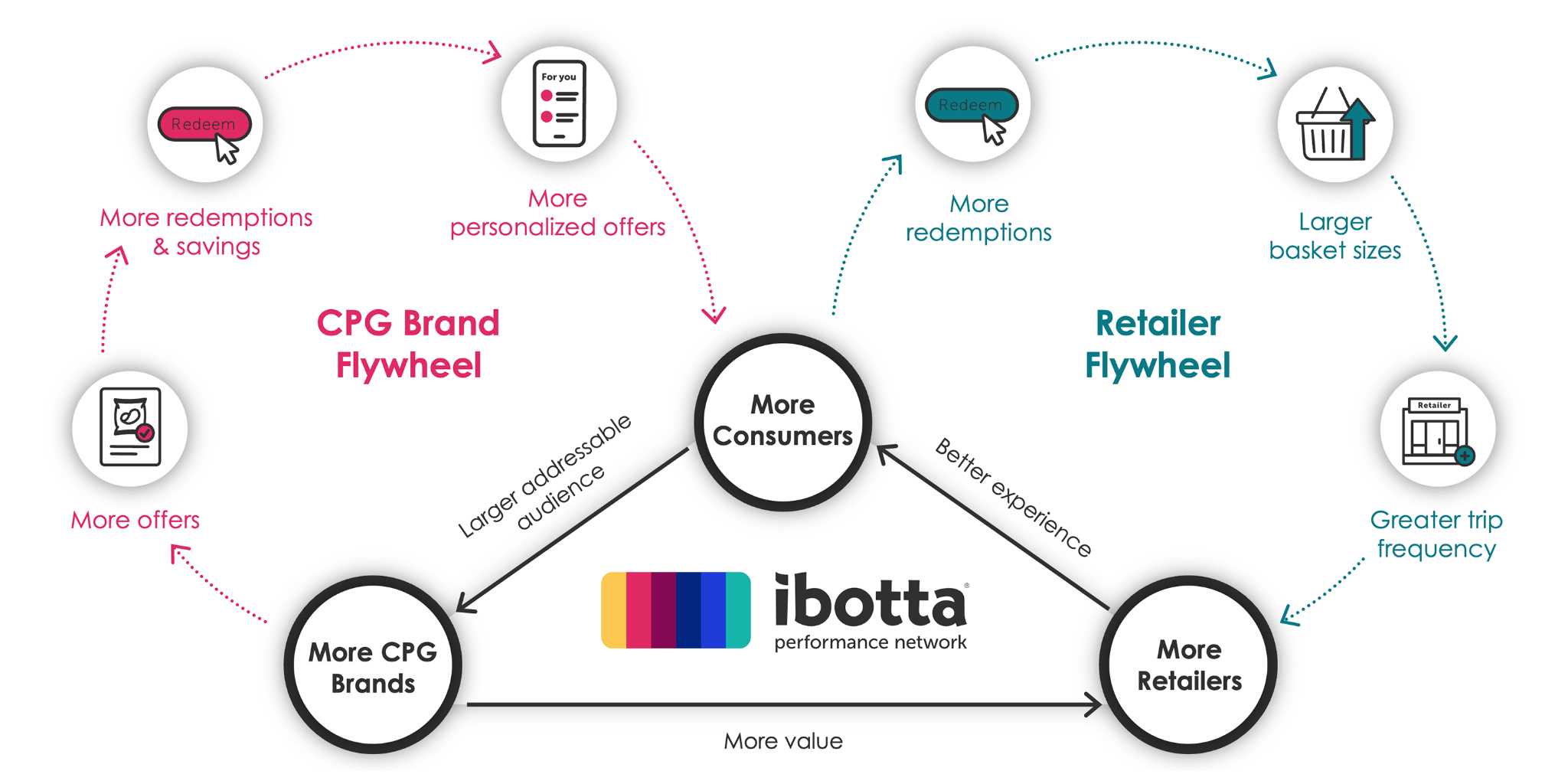

The above components of our network work together to create interconnected flywheels that can over time strengthen and accelerate the value of the IPN for our constituents.

CPG brand flywheel. The more offers CPG brands sponsor, the greater value we are able to deliver to consumers, and the more likely that they continue to engage with and recommend our offers to friends. The more consumers engage, the more investment we receive from both new and existing CPG brands that are eager to influence the greater spending power of this audience.

Retailer flywheel. As retailers make offers easier to redeem, more consumers use them, which in turn attracts greater investments in offers from CPG brands, which ultimately results in more consumers using the retailer’s loyalty program.

8

Our Competitive Strengths

We believe the following attributes and capabilities represent our core strengths and provide us with valuable competitive advantages.

“One-stop shop” for national promotions. Ibotta provides CPG brands with a comprehensive solution that simplifies and streamlines the entire digital promotions process from end-to-end.

Shared success model that aligns our incentives with our clients’ incentives. Our innovative fee-per-sale model increases the cost efficiency of digital marketing within the CPG industry. We only make money when CPG brands make money, and this alignment of incentives creates trust and encourages them to invest more on the IPN over time.

Audience scale capable of moving substantial sales volumes for clients. Built over a decade, the IPN represents the largest item-level network of CPG brands, publishers, and consumers in the digital promotion space. We believe this scale positions the IPN as a viable alternative to top-of-funnel media tactics such as TV and programmatic media.

Ability to access national promotions budgets, leveraging our large D2C business. Ibotta’s sales team has over a decade of experience building relationships with thousands of CPG brands and sourcing offers for placement on our widely used app, and more recently for distribution across our broader network. This gives Ibotta an advantage in winning business with new retailer publishers because our competitors cannot match the same volume of incremental, national offers.

Strong partner network that includes leading retailers. As CPG brands place promotions on the IPN, their products place pressure on those brands’ competitors to engage with Ibotta to help them remain competitive. We believe this bandwagon effect has and will continue to help Ibotta grow revenue with clients.

Single source of truth for coordinated offer delivery. Before the introduction of the IPN, CPG brands had to stagger their digital promotions to prevent them from overlapping or being stacked with each other. The IPN made it possible for CPG brands to deliver digital promotions across retailers without the risk that their promotions could be redeemed in more than one publisher environment for a single purchase.

Powerful AI-driven technology that leverages a highly differentiated data set. We use cloud-based, serverless technology to ingest and process vast amounts of cross-retailer, item-level purchase data. This valuable dataset powers our proprietary AI models and helps us get better and better at recommending the right offers to consumers and creating the right types of offers for our clients.

Privacy-compliant approach to digital marketing. The core of Ibotta’s solution does not rely on third-party cookies for targeting and measurement. Instead, consumers voluntarily provide their purchase data in order to receive rewards and personalized offers.

Ibotta’s Value Proposition

Value for CPG brands

•Grow market share efficiently through success-based marketing at-scale

•Drive verified incremental sales

•Enable seamless, coordinated campaign execution and measurement

•Receive valuable data and insights

9

Value for Publishers

•Drive more revenue and consumer engagement through differentiated rewards content

•Grow revenue from Retail Media Networks (RMNs)

•Build customer loyalty by enabling closed-loop rewards instead of discounts

•Reduce time and investment for building and maintaining a rewards infrastructure

•Receive valuable ongoing consultation regarding rewards best practices

Value for Consumers

•Receive savings on everyday items

•Earn rewards easily through seamless, convenient, and intuitive digital interfaces

Growth Strategies

We intend to capitalize on our large market opportunity with the following key growth strategies.

Grow our audience. To deliver more redemptions in the future, we plan to reach more consumers with our digital offers. Ibotta will seek to continue to grow the audience that we reach through the IPN through increased penetration at existing publishers and by adding to the network of third-party publishers.

•Grow redeemers on existing third-party publisher properties. We believe there is significant opportunity to grow the audience at existing third-party publishers.

•Add new third-party publishers in grocery. We are focused on expanding our audience by building new partnerships with retailers.

•Expand into new categories of publishers. In addition to expanding within the grocery channel, Ibotta may also seek to publish its content on the properties of delivery service providers, specialty retailers, and other, non-retailer publishers.

Add offers. We have observed a strong correlation between the offers we make available to consumers and the number of redemptions we generate. We will seek to grow investment from our existing CPG brands, while also seeking to expand into new brands and categories.

•Grow investment from current clients. Within each client that invests in Ibotta today, we believe there is a significant opportunity to grow their budget invested to keep up with the growth of our audience. Additionally, many of our clients have multiple brands within their portfolio, and we only service a subset of those brands today.

•Expand our client base. While we already work with many of the CPG companies in the United States, there are still many CPG companies that do not yet use our services. Additionally, we have significant untapped opportunities in general merchandise categories such as toys, clothing, beauty, electronics, pet, home goods, and sporting goods.

•Continue to enhance the IPN through innovation. We will continue to invest in technology to further develop and accelerate the growth of the IPN for CPG brands, publishers, and consumers. As the data generated by the IPN grows, we believe Ibotta will generate more valuable insights about purchase behavior and market trends and may be able to automatically optimize recommendations for consumers as well as campaigns for clients based on real-time data from across the network.

10

Risk Factors Summary

Our business is subject to numerous risks and uncertainties that you should consider before investing in our Company. These risks are described more fully in the section titled “Risk Factors” in this prospectus. These risks include, but are not limited to, the following:

•We have a history of net losses, we anticipate increasing expenses in the future, and we may not be able to attain profitability in the future.

•Our business, financial condition, results of operations, and prospects will be adversely affected if we do not renew, maintain, and expand our relationships with existing publishers and add new publishers to the IPN.

•We are also dependent on our publishers to take steps to integrate with the IPN and to maximize and encourage offer redemption, including decisions relating to user experience and design, marketing, and proper maintenance of their technology.

•If we fail to maintain or grow offer redemptions on our network, our revenues and business may be negatively affected.

•Our business, financial condition, results of operations, and prospects will suffer if CPG brands do not use our network for digital promotions.

•We may not be able to sustain our revenue growth rate in the future.

•We provide content to publishers indirectly through third-party technology partners and our business, financial condition, results of operations, and prospects will be adversely affected if we do not renew, maintain and expand our relationships with such third-party technology partners.

•We expect a number of factors to cause our results of operations to fluctuate on a quarterly and annual basis, which may make it difficult to predict our future performance.

•Macroeconomic conditions, including slower growth or a recession and supply chain disruptions, have previously and could continue to adversely affect our business, financial condition, results of operations, and prospects.

•Competition presents an ongoing threat to the success of our business.

•Our business, financial condition, results of operations, and prospects will suffer if we do not renew, maintain and expand our relationships with retailers.

•If we fail to effectively manage our growth, our business, financial condition, results of operations, and prospects could be adversely affected.

•We have a limited operating history and operate in an evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful.

•We are making substantial investments in our technologies, and if we do not continue to innovate and further develop our platform, our platform developments do not perform, or we are not able to keep pace with technological developments, we may not remain competitive, and our business and results of operations could suffer.

•We have previously identified material weaknesses in our internal controls over financial reporting and if we are unable to maintain effective internal controls or if we identify additional material weaknesses in the future, we may not be able to accurately or timely report our financial condition or results of operations, which may adversely affect our business, financial condition, results of operations, and prospects.

11

•The dual class stock structure of our common stock will have the effect of concentrating voting control with Bryan Leach, our Founder, Chief Executive Officer and President and a member of our board of directors, which will generally preclude your ability to influence the outcome of matters submitted to our stockholders for approval, subject to limited exceptions, including the election of our board of directors, the adoption of amendments to our certificate of incorporation and bylaws (where adopted by stockholders), and the approval of any merger, consolidation, sale of all or substantially all of our assets, or other major corporate transactions.

•Although we do not expect to rely on the “controlled company” exemption under the listing standards of the , we expect to have the right to use such exemption and therefore we could in the future avail ourselves of certain reduced corporate governance requirements.

Corporate Information

We were incorporated in 2011 as Zing Enterprises, Inc., a Delaware corporation. In 2012, we changed our name to Ibotta, Inc. Our principal executive office is located at 1801 California Street, Suite 400, Denver, Colorado 80202, and our telephone number is 303-593-1633. Our website address is https://www.ibotta.com. Information contained on, or that can be accessed through, our website is not incorporated by reference into this prospectus and should not be considered to be part of this prospectus.

We use Ibotta, the Ibotta logo, the IPN logo, and other marks as trademarks in the United States. This prospectus contains references to our trademarks and service marks and to those belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus, including logos, artwork, and other visual displays, may appear without the ® or TM symbols, but such references are not intended to indicate in any way that we will not assert, to the fullest extent under applicable law, our rights, or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other entities’ trade names, trademarks, or service marks to imply an endorsement or sponsorship of us by any other entity.

Status as a Controlled Company

As a result of our dual class common stock structure, Bryan Leach, our Founder, Chief Executive Officer and President and a member of our board of directors, and entities affiliated with Mr. Leach, will be able to exercise voting control with respect to an aggregate of shares of our Class B common stock, representing approximately % of the total voting power of our outstanding capital stock as of . Mr. Leach will have the authority to vote the shares of Class B common stock at his discretion on all matters to be voted upon by stockholders. Therefore, we will be considered a “controlled company” as that term is set forth in the listing standards of the . Under these listing standards, a company in which over 50% of the voting power for the election of directors is held by an individual, a group, or another company is a “controlled company” and may elect not to comply with certain listing standards of the regarding corporate governance including the requirements (1) that a majority of our board of directors consist of independent directors, (2) the compensation committee and nominating and corporate governance committee be comprised entirely of independent members and (3) to make the charters for each of the compensation committee and nominating and corporate governance committee available on the Company’s website. These requirements would not apply to us if, in the future, we choose to avail ourselves of the “controlled company” exemption. Although we qualify as a “controlled company,” we do not currently expect to rely on these exemptions and intend to fully comply with all corporate governance requirements under the listing standards of the .

However, if we were to utilize some or all of these exemptions, we would not comply with certain of the corporate governance standards of the , which could adversely affect the protections for other stockholders.

In addition, our “controlled company” status will generally preclude our stockholders’ ability to influence the outcome of matters submitted to our stockholders for approval, subject to limited exceptions, including the election of our board of directors, the adoption of amendments to our certificate of

12

incorporation and bylaws (where adopted by stockholders), and the approval of any merger, consolidation, sale of all or substantially all of our assets, or other major corporate transactions.

Implications of Being an Emerging Growth Company

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended (JOBS Act). We will remain an emerging growth company until the earliest to occur of: (i) the last day of the fiscal year in which we have more than $1.235 billion in annual revenue; (ii) the date we qualify as a “large accelerated filer,” with at least $700 million of equity securities held by non-affiliates; (iii) the date on which we have issued, in any three-year period, by us of more than $1.0 billion in non-convertible debt securities; and (iv) the last day of the fiscal year ending after the fifth anniversary of our initial public offering.

As a result of this status, we have elected to take advantage of reduced reporting requirements in the registration of which this prospectus forms a part and may elect to take advantage of other reduced reporting requirements in our future filings with the Securities and Exchange Commission (SEC). In particular, in this prospectus we have not included all of the executive compensation-related information that would be required if we were not an emerging growth company. In addition, the JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards, delaying the adoption of these accounting standards until they would apply to private companies. We intend to elect to use this extended transition period to enable us to comply with new or revised accounting standards that have different effective dates for public and private companies until the earlier of the date we (i) are no longer an emerging growth company or (ii) affirmatively and irrevocably opt out of the extended transition period provided in the JOBS Act. As a result, our financial statements may not be comparable to companies that comply with the new or revised accounting standards as of public company effective dates.

13

THE OFFERING

Class A common stock offered by us |

shares |

|||||||

Class A common stock to be outstanding immediately after this offering |

shares (or shares if the underwriters exercise their option to purchase additional shares of common stock in full). |

|||||||

| Class B common stock to be outstanding immediately after this offering | shares |

|||||||

Class A and B common stock to be outstanding immediately after this offering |

shares |

|||||||

Option to purchase additional shares |

We have granted the underwriters an option exercisable for a period of 30 days to purchase up to additional shares of our Class A common stock. |

|||||||

Use of proceeds |

We estimate that the net proceeds to us from the sale of the shares of our Class A common stock in this offering will be approximately $ million, or approximately $ million if the underwriters exercise their option to purchase additional shares in full, based upon an assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us.

We intend to use the net proceeds we receive from this offering for general corporate purposes, including working capital, operating expenses, and capital expenditures. See the section titled “Use of Proceeds” for more information.

|

|||||||

Risk factors |

See the section titled “Risk Factors” and other information for a discussion of factors you should carefully consider before deciding to invest in shares of our Class A common stock.

|

|||||||

14

Voting Rights |

We will have two series of common stock: Class A common stock and Class B common stock. Shares of Class A common stock are entitled to one vote per share. Shares of Class B common stock are entitled to twenty votes per share.

Holders of our Class A common stock and Class B common stock will generally vote together as a single series, unless otherwise required by law or our amended and restated certificate of incorporation. Upon completion of this offering, Bryan Leach, our Founder, Chief Executive Officer and President and a member of our board of directors, and entities affiliated

with Mr. Leach will hold approximately % of the voting power of our outstanding capital stock in the aggregate, which voting power may increase over time as Mr. Leach’s equity awards which are outstanding at the time of the completion of this offering are exercised or vested. If all such equity awards held by Mr. Leach had been exercised or vested and exchanged for shares of Class B common stock as of the date of the completion of this offer, Mr. Leach and entities affiliated with Mr. Leach would collectively hold % of the voting power of our outstanding capital stock. As a result, Mr. Leach generally will be able to determine any action requiring the approval of our stockholders, subject to limited exceptions, including the election of our board of directors, the adoption of amendments to our certificate of incorporation and bylaws (where adopted by stockholders), and the approval of any merger, consolidation, sale of all or substantially all of our assets, or other major corporate transactions. Additionally, our executive officers, directors, and holders of 5% or more of our capital stock will hold, in the aggregate, approximately % of the voting power of our outstanding capital stock following this offering. See the sections titled “Principal Stockholders” and “Description of Capital Stock” for additional information.

|

|||||||

Proposed trading symbol |

“IBTA” |

|||||||

The number of shares of our Class A common stock and Class B common stock to be outstanding after this offering is based on shares of our Class A common stock and shares of our Class B common stock outstanding as of December 31, 2023 after giving effect to the Capital Stock Conversion, Reclassification, and Class B Stock Exchange (each as described below), as if they had occurred on December 31, 2023, and reflects:

• shares of our convertible preferred stock that will automatically convert into an equal number of shares of our common stock immediately prior to the effectiveness of the filing of our amended and restated certificate of incorporation filed in connection with this offering. We refer to this conversion of our convertible preferred stock into common stock as the Capital Stock Conversion;

• shares of common stock outstanding, which shares will be reclassified into an equal number of shares of Class A common stock in connection with the filing of our amended and restated certificate of incorporation filed in connection with this offering. We refer to this reclassification of our common stock into Class A common stock as the Reclassification; and

15

• shares of our Class B common stock outstanding after giving effect to the Reclassification, which reflects shares of our Class A common stock outstanding and beneficially owned by Bryan Leach and certain related entities as of December 31, 2023 that will be exchanged for an equivalent number of shares of our Class B common stock following the effectiveness of the filing of our amended and restated certificate of incorporation filed in connection with this offering (Class B Stock Exchange).

The number of shares of our Class A common stock and Class B common stock to be outstanding as of December 31, 2023 after giving effect to the Capital Stock Conversion, Reclassification, and Class B Stock Exchange, as if they had occurred on December 31, 2023, excludes the following:

• shares of our Class A common stock issuable upon exercise of options to purchase shares of our Class A common stock outstanding as of December 31, 2023 under our 2011 Equity Incentive Plan (2011 Plan), at a weighted average exercise price of $ per share;

• shares of our Class A common stock issuable upon the exercise of options to purchase shares of our Class A common stock that we granted after December 31, 2023 under our 2011 Plan, at an exercise price of $ per share;

• shares of our Class A common stock issuable upon the exercise of options to purchase shares of our Class A common stock that we granted after December 31, 2023 under our 2011 Plan, at an exercise price of $ per share to Bryan Leach that can be exchanged for an equivalent number of shares of Class B common stock pursuant to the Equity Award Exchange Agreement (as defined below);

• shares of Class A common stock reserved for future issuance under our 2011 Plan as of December 31, 2023, which shares will be added to the shares to be reserved for issuance under our 2024 Equity Incentive Plan (2024 Plan), which will become effective on the business day immediately prior to the date of effectiveness of the registration statement of which this prospectus forms a part;

• shares of our Class A common stock reserved for future issuance under our 2024 Plan as well as any automatic increases in the number of shares of our Class A common stock reserved for future issuance under the 2024 Plan;

• shares of our Class A common stock to be reserved for future issuance under our 2024 Employee Stock Purchase Plan (ESPP), which will become effective on the business day immediately prior to the date of effectiveness of the registration statement of which this prospectus forms a part, as well as any automatic increases in the number of shares of our Class A common stock reserved for future issuance under the ESPP; and

• shares of Class A common stock, following the issuance of shares of our Class A common stock upon the automatic conversion of the convertible notes, based upon an assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, and after taking into account option grants made following the issuance of Class A common stock warrants (Walmart Warrant) held by Walmart. The vesting and exercise terms of the Walmart Warrant are further described in the section titled “Certain Relationships and Related Party Transactions—Agreements with Walmart.”

Following the completion of this offering and pursuant to an equity award exchange agreement (Equity Award Exchange Agreement) to be entered into between us and Bryan Leach, our Founder, Chief Executive Officer and President, Mr. Leach shall have a right (but not an obligation) to require us to exchange any shares of Class A common stock received upon the exercise of outstanding options to purchase shares of Class A common stock for an equivalent number of shares of Class B common stock. We refer to this right as the Equity Award Exchange. The Equity Award Exchange applies only to equity awards granted to Mr. Leach prior to the effectiveness of the filing of our amended and restated certificate

16

of incorporation. As of , there were shares of our Class A common stock subject to options held by Mr. Leach under our 2011 Plan that may be exchanged, upon exercise, for an equivalent number of shares of our Class B common stock following this offering.

Unless otherwise indicated, this prospectus reflects and assumes the following:

•the Capital Stock Conversion will occur immediately prior to the effectiveness of our amended and restated certificate of incorporation in Delaware filed in connection with this offering;

•the filing and effectiveness of our amended and restated certificate of incorporation in Delaware and the effectiveness of our amended and restated bylaws will each occur prior to the completion of this offering and will effect the Reclassification of our common stock into Class A common stock;

•the Class B Stock Exchange will occur immediately following the effectiveness of our amended and restated certificate of incorporation in Delaware, and the completion of this offering will occur following the Class B Stock Exchange;

• shares of our Class A common stock issuable upon the automatic conversion of $ million in convertible unsecured subordinated promissory notes, which will occur concurrently upon the closing of this offering, which we refer to as the Notes Conversion, based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, the conversion terms which are further described in the section titled, “Certain Relationships and Related Party Transactions—2022 Promissory Notes”;

•the effectiveness of a -for-1 stock split of our capital stock to be effected on ;

•no exercise of outstanding options after December 31, 2023; and

•no exercise by the underwriters of their option to purchase additional shares of Class A common stock from us in this offering.

17

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables summarize our consolidated financial and other data. We have derived the summary consolidated statement of operations data for 2023 and 2022 and summary consolidated balance sheet data as of December 31, 2023 from our audited consolidated financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future. The following summary consolidated financial and other data should be read in conjunction with the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our consolidated financial statements and the related notes, and our unaudited condensed combined statement of operations included elsewhere in this prospectus.

Year ended December 31, |

|||||||||||

2023 |

2022 |

||||||||||

(in thousands, except share amounts and per share amounts) |

|||||||||||

Consolidated Statements of Operations Data: |

|||||||||||

Revenue |

$ |

$ | 210,702 | ||||||||

Cost of revenue |

46,176 | ||||||||||

Gross profit |

164,526 | ||||||||||

Operating expenses: |

|||||||||||

Sales and marketing |

110,069 | ||||||||||

Research and development |

42,558 | ||||||||||

General and administrative |

49,164 | ||||||||||

Depreciation and amortization |

3,048 | ||||||||||

Total operating expenses |

204,839 | ||||||||||

Loss from operations |

(40,313) | ||||||||||

Other expense, net |

(14,286) | ||||||||||

Loss before provision for income taxes |

(54,599) | ||||||||||

Provision for income taxes |

(262) | ||||||||||

Net loss |

$ |

$ | (54,861) | ||||||||

Net loss per share: |

|||||||||||

Basic |

(6.33) | ||||||||||

Diluted |

(6.33) | ||||||||||

Weighted average common shares outstanding: |

|||||||||||

Basic |

8,672,426 | ||||||||||

Diluted |

8,672,426 | ||||||||||

Pro forma net loss per share attributable to common stockholders, basic and diluted (1)

|

|||||||||||

Pro forma weighted average common shares outstanding, basic and diluted (1)

|

|||||||||||

______________

(1)See Note to our consolidated financial statements as of and for the year ended December 31, 2022 and Note to our financial statements as of and for the year ended December 31, 2023 included elsewhere in this prospectus for an explanation of the method used to calculate historical and pro forma net loss per share, basic and diluted, and the weighted average number of shares of common stock used in the computation of the per share amounts.

18

As of December 31, 2023 |

|||||||||||||||||

Actual |

Pro Forma (1)

|

Pro Forma As Adjusted (2) (3)

|

|||||||||||||||

(in thousands) |

|||||||||||||||||

Consolidated Balance Sheet Data: |

|||||||||||||||||

Cash and cash equivalents |

$ |

$ |

$ |

||||||||||||||

Short-term investments |

|||||||||||||||||

Working capital (4)

|

|||||||||||||||||

Total assets |

|||||||||||||||||

Current liabilities |

|||||||||||||||||

Convertible notes |

|||||||||||||||||

Total liabilities |

|||||||||||||||||

Redeemable convertible preferred stock |

|||||||||||||||||

Accumulated deficit |

|||||||||||||||||

Total stockholders’ deficit |

|||||||||||||||||

______________

(1)The pro forma column in the consolidated balance sheet data table above reflects (i) the Capital Stock Conversion, as if such conversion had occurred on December 31, 2023; (ii) the Reclassification, as if such Reclassification had occurred on December 31, 2023; (iii) the Class B Stock Exchange, as if such stock exchange had occurred on December 31, 2023; (iv) the Notes Conversion, as if such conversion had occurred on December 31, 2023 and (v) the filing and effectiveness of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws prior to the completion of this offering.

(2)The pro forma as adjusted column in the consolidated balance sheet data table above gives effect to (i) the pro forma adjustments set forth in note 1 above, and (ii) the sale and issuance by us of shares of our Class A common stock in this offering, based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us.